7.5: Inflation Pros and Cons

- Page ID

- 250517

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Economic Problems Associated with Inflation

Inflation can cause redistributions of purchasing power that hurt some and help others. People who are hurt by inflation include those who are holding a lot of cash, whether it is in a safe deposit box or in a cardboard box under the bed. When inflation happens, the buying power of cash is diminished. But cash is only an example of a more general problem: anyone who has financial assets invested in a way that the nominal return does not keep up with inflation will tend to suffer from inflation.

For example, if a person has money in a bank account that pays 4% interest, but inflation rises to 5%, then the real rate of return for the money invested in that bank account is negative 1%. The problem of a good-looking nominal interest rate being transformed into an ugly-looking real interest rate can be worsened by taxes. The U.S. income tax is charged on the nominal interest received in dollar terms, without an adjustment for inflation. So, a person who invests $10,000 and receives a 5% nominal rate of interest is taxed on the $500 received — no matter whether the inflation rate is 0%, 5%, or 10%. If inflation is 0%, then the real interest rate is 5% and all $500 is a gain in buying power. But if inflation is 5%, then the real interest rate is zero and the person had no real gain — but owes income tax on the nominal gain anyway. If inflation is 10%, then the real interest rate is negative 5% and the person is actually falling behind in buying power, but would still owe taxes on the $500 in nominal gains. Inflation can cause unintended redistributions for wage earners, too. Wages do typically creep up with inflation over time eventually. (15)

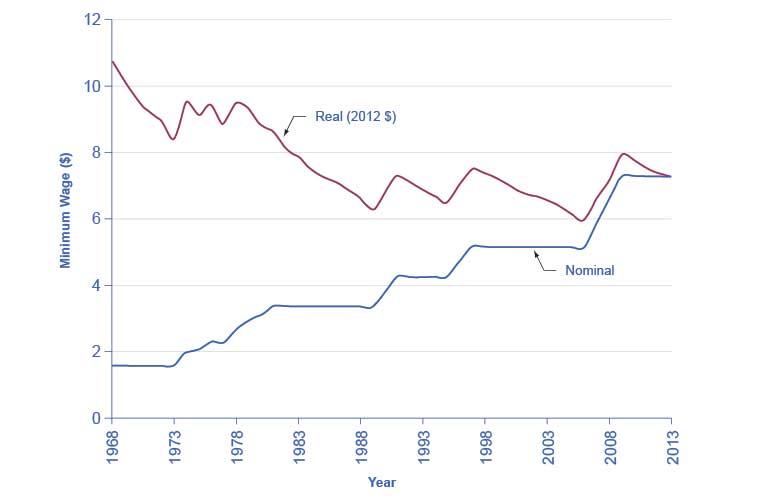

U.S. Minimum Wage and Inflation

The average hourly wage in the U.S. economy increased from $3.23 in 1970 to $19.20 in 2012, which is an increase by a factor of almost six. Over that time period, the Consumer Price Index increased by an almost identical amount. However, increases in wages may lag behind inflation for a year or two, since wage adjustments are often somewhat sticky and occur only once or twice a year. Moreover, the extent to which wages keep up with inflation creates insecurity for workers and may involve painful, prolonged conflicts between employers and employees. If the minimum wage is adjusted for inflation only infrequently, minimum wage workers are losing purchasing power from their nominal wages, as shown in Figure 5.3.

After adjusting for inflation, the federal minimum wage dropped more than 30 percent from 1967 to 2010, even though the nominal figure climbed from $1.40 to $7.25 per hour. Increases in the minimum wage in between 2008 and 2010 kept the decline from being worse — as it would have been if the wage had remained the same as it did from 1997 through 2007. (15)

Economic Problems Associated with Inflation (Cont’d)

Retirees often receive a large share of their income in a form that does not increase over time. Most pensions have traditionally been set as a fixed nominal dollar amount per year at retirement. For this reason, pensions are called “defined benefits” plans. Even if inflation is low, the combination of inflation and a fixed income can create a substantial problem over time. A person who retires on a fixed income at age 65 will find that losing just 1% to 2% of buying power per year to inflation compounds to a considerable loss of buying power after a decade or two.

Fortunately, pensions and other defined benefits retirement plans are rare, and replaced instead by “defined contribution” plans, such as 401(k)s and 403(b)s. In these plans, the employer contributes a fixed amount to the worker’s retirement account on a regular basis (usually every pay check). To the extent that the investments made generate real rates of return, retirees do not suffer from the inflation costs of traditional pensioners.

However, ordinary people can sometimes benefit from the unintended redistributions of inflation. Consider someone who borrows $10,000 to buy a car at a fixed interest rate of 9%. If inflation is 3% at the time the loan is made, then the loan must be repaid at a real interest rate of 6%. But if inflation rises to 9%, then the real interest rate on the loan is zero. In this case, the borrower’s benefit from inflation is the lender’s loss. A borrower paying a fixed interest rate, who benefits from inflation, is just the flip side of an investor receiving a fixed interest rate, who suffers from inflation.

The unintended redistributions of buying power caused by inflation may have a broader effect on society. When inflation causes a retiree who built up a pension or invested at a fixed interest rate to suffer, however, while someone who borrowed at a fixed interest rate benefits from inflation, it is hard to believe that this outcome was deserved in any way. Similarly, when homeowners benefit from inflation because the price of their homes rises, while renters suffer because they are paying higher rent, it is hard to see any useful financial benefits. One of the reasons that inflation is so disliked by the general public is a sense that it makes economic rewards and penalties more arbitrary, and therefore likely to be perceived as unfair. (15)

Benefits of Inflation

Although the economic effects of inflation are primarily negative, two counteracting points are worth noting.

First, the impact of inflation will differ considerably according to whether it is creeping up slowly at 0% to 2% per year, galloping along at 10% to 20% per year, or racing to the point of hyperinflation at, say, 40% per month. Hyperinflation can rip an economy and a society apart. An annual inflation rate of 2%, 3%, or 4%, however, is a long way from a national crisis. Low inflation is also better than deflation, which occurs with severe recessions.

Second, an argument is sometimes made that moderate inflation may help the economy by making wages in labor markets more flexible. This argument may, however, be controversial. A full analysis would have to take all the effects of inflation into account. It does, however, offer another reason to believe that, all things considered, very low rates of inflation may not be especially harmful. (15)

- Principles of Macroeconomics. Authored by: OpenStax. Located at: http://cnx.org/contents/4061c832-098e-4b3c-a1d9-7eb593a2cb31@11.11. License: CC BY: Attribution